House Mortgages: What You Need To Know

Article writer-Kragelund McCoyWhile everyone considers buying a home at some point in their life, having to get a mortgage to pay for it can seem intimidating. In fact, some people are so worried about the situation that they continue to rent instead. Build your confidence by reading this article and learning about mortgages.

Try to have a down payment of at least 20 percent of the sales price. In addition to lowering your interest rate, you will also avoid pmi or private mortgage insurance premiums. This insurance protects the lender should you default on the loan. Premiums are added to your monthly payment.

Work with your bank to become pre-approved. Pre-approval helps give you an understanding of how much home you can really afford. It'll keep you from wasting time looking at houses that are simply outside of your range. It'll also protect you from overspending and putting yourself in a position where foreclosure could be in your future.

Get your documents ready before you go to a mortgage lender. You should have an idea of the documents they will require, and if you don't, you can ask ahead of time. Most mortgage lenders will want the same documents, so keep them together in a file folder or a neat stack.

Find out how much your mortgage broker will be making off of the transaction. Many times mortgage broker commissions are negotiable just like real estate agent commissions are negotiable. Get this information and writing and take the time to look over the fee schedule to ensure the items listed are correct.

Lenders look at your debt-to-income ratio in order to determine if you qualify for a loan. If your total debt is over a certain percentage of your income, you may have trouble qualifying for a loan. Therefore, reduce your debt by paying off your credit cards as much as you can.

Look into no closing cost options. If closing costs are concerning you, there are many offers out there where those costs are taken care of by the lender. The lender then charges you slightly more in your interest rate to make up for the difference. This can help you if immediate cash is an issue.

When considering https://www.bizjournals.com/sacramento/news/2022/01/10/acquisition-of-suncrest-bank-completed.html , check the lender's record with the Better Business Bureau (BBB). https://www.thetimes.co.uk/money-mentor/article/bank-switching-bonuses/ is an excellent resource for learning what your potential lender's reputation is. Unhappy customers can file a complaint with the BBB, and then the lender gets the opportunity to address the complaint and resolve it.

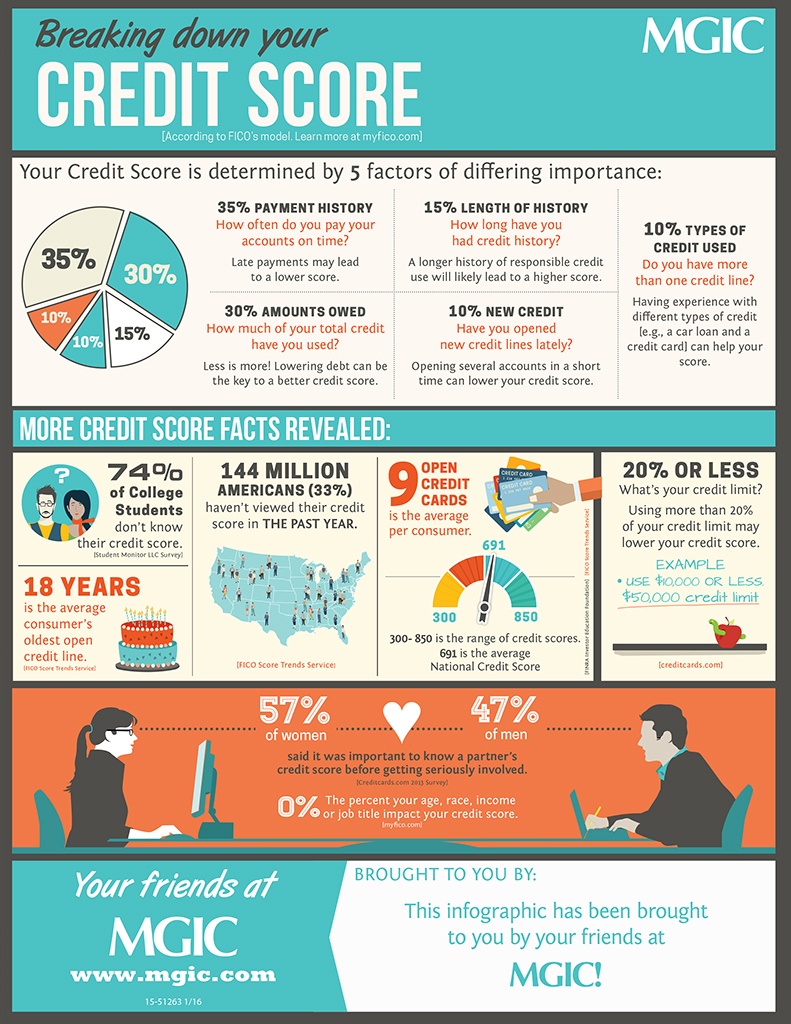

A good credit score is essential if you want to finance a home. If your score is below 600 you have some work to do before you can hope to purchase a home. Begin by getting a copy of your credit record and verifying that all the information on it is correct.

Shop around for the best mortgage terms. Lenders individually set term limits on their loans. By shopping around, you can get a lower interest rate or lower down payment requirements. When shopping around, don't forget about mortgage brokers who have the ability to work with multiple lenders to find you the best rate.

Take the time to get your credit into the best shape possible before you look into getting a home mortgage. The better the shape of your credit rating, the lower your interest rate will be. This will mean paying thousands less over the term of your mortgage contract, which will be worth the wait.

Be realistic when choosing a home. Just because your lender pre-approves you for a certain amount doesn't mean that's the amount you can afford. Look at your income and your budget realistically and choose a home with payments that are within your means. This will save you a lifetime of stress in the long run.

Monitor interest rates before signing with a mortgage lender. If the interest rates have been dropping recently, it may be worth holding off with the mortgage loan for a few months to see if you get a better rate. Yes, it's a gamble, but it has the potential to save a lot of money over the life of the loan.

When shopping for a mortgage loan, ask if the rate is adjustable or fixed. Adjustable rate loans have interest rates which can vary greatly during the life of the mortgage. Also, your monthly payments will never be fixed and can increase by hundreds of dollars monthly. If the rate on the loan is adjustable, ask how and when the loan payment and rate could change.

Pay your mortgage down faster to free up money for the future. Pay a little extra each month when you have some extra savings. When you pay the extra each month, make sure to let the bank know the over-payment is for the principal. You do not want them to put it towards the interest.

Set a solid relationship with your bank or lender in the year preceding applying for a mortgage loan. You may find it helpful to get a personal loan and pay it off before making a home loan application. This shows them that your are a reliable borrower.

Look into a mortgage that requires payment every two weeks as opposed to monthly. This will let you make more payments every year, greatly reducing the amount of money you spend on interest on the life of the loan. This works well if your pay period is every two weeks since the payments can be automatically drawn from your bank.

If you want to refinance your mortgage, you will be responsible for closing costs. Do some calculations to see when you will break even. If you do not plan to stay at your house for much longer, it may not be worth your while if you have to pay a lot of fees to refinance.

As was stated in the introductory paragraph of this article, the mortgage financing process is very complicated. It can seem indecipherable to a real estate novice. The key to financing a great mortgage that allows you to buy the home of your dreams is to educate yourself on the mortgage process. Study the mortgage tips and advice in this article very carefully.